Insurers look at your roof’s material, condition, and age to assess the risk of damage and determine your homeowners insurance rates. Your roof isn’t just a cosmetic feature it’s your home’s first defense against weather, and its ability to withstand hazards like wind, hail, fire, and heavy snow plays a major role in whether you’re considered a low- or high-risk policyholder. The sturdier, longer-lasting, and more hazard-appropriate your roof is, the more favorable your insurance terms are likely to be.

This guide explains why roof type affects insurance, compares how common materials are viewed by insurers, outlines other key evaluation factors, and shares simple tips to make your roof more appealing for coverage. Let's look at roof types for insurance purposes. What do insurers look for?

Your roof is a critical factor in determining your home’s risk level and overall insurability. Because it’s the first line of defense against costly damage from weather and other hazards, insurers closely evaluate its type, condition, and expected performance. The stronger and more durable the roof, the more confidence an insurer has in offering better rates and broader coverage.

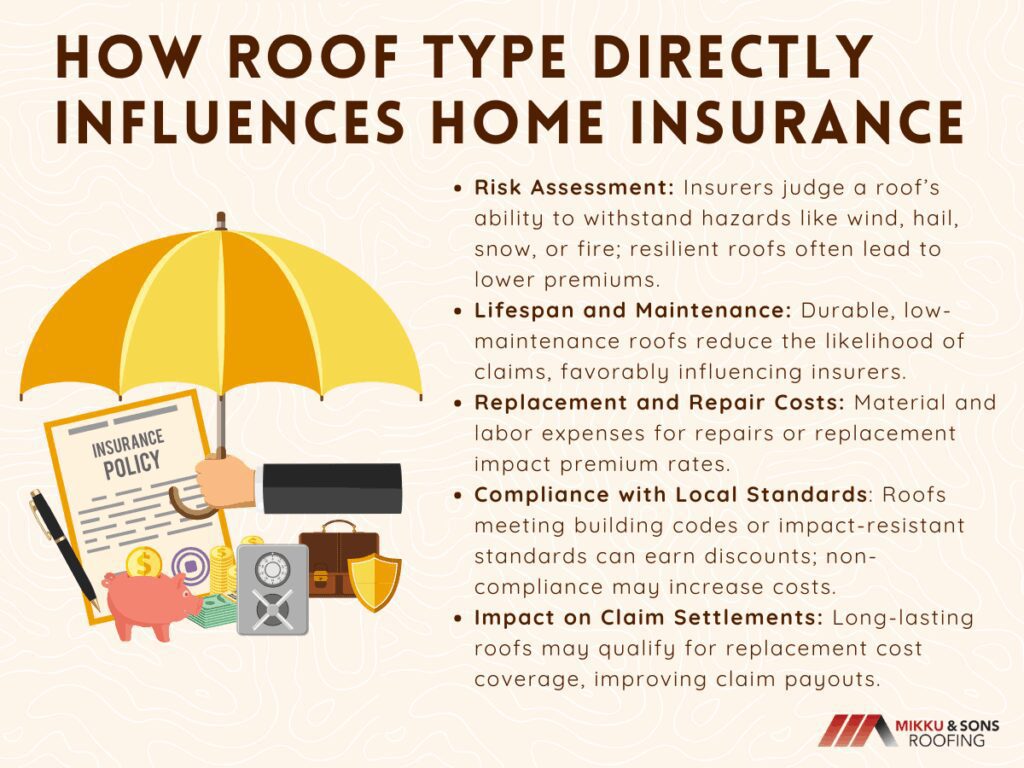

Insurers evaluate roof type to estimate its ability to withstand hazards like wind, hail, snow, or fire. Roofs with proven resilience in your local climate are considered lower risk, often resulting in reduced premiums and better policy terms.

A roof’s expected longevity and upkeep requirements directly influence the likelihood of claims. Durable, low-maintenance roofs suggest fewer potential repairs, which insurers view favorably.

Even strong roofs can be costly to replace or repair after damage. Insurers factor in material and labor expenses when determining premium rates.

Roofs that meet or exceed local building codes—such as impact-resistant standards in hail-prone areas—are often rewarded with discounts. Non-compliant roofs can lead to higher costs or limited coverage.

Certain roof types and ages qualify for replacement cost coverage, while others may be settled at actual cash value. Choosing a long-lasting, resilient roof can improve the payout terms in the event of a claim.

A roof is more than just a shelter—it’s a major component in your insurance risk profile. By understanding what insurers value in a roof, you can make decisions that enhance both your home’s protection and your policy’s affordability.

Your choice of roofing material not only impacts your home’s appearance and structural protection but also plays a direct role in how your insurance policy is priced and structured. Each roof type comes with its own strengths, weaknesses, and risk profile in the eyes of insurers.

Asphalt shingles are the most common and affordable roofing option, with a lifespan of about 15–30 years. While they offer decent weather resistance, they are more susceptible to hail, wind, and granule loss over time, which can lead to more frequent claims. Insurers typically treat them as a standard risk, but premiums may be higher in storm-prone areas.

Metal roofing is highly durable, lasting 40–70 years, and offers excellent resistance to wind, hail, and fire. Its longevity and low maintenance needs often make it a favorite with insurers, especially in wildfire or severe weather zones. However, higher installation costs and potential denting from large hail can slightly offset these benefits in premium calculations.

Clay and concrete tiles are known for their exceptional fire resistance and long lifespan of 50–100 years. They are ideal for hot or fire-prone climates but can crack easily under impact and require strong structural support due to their weight. Insurers often view them positively for fire safety but factor in the high replacement costs when setting rates.

Slate is among the most durable roofing materials, lasting 75–200 years with minimal upkeep. Its fire resistance and resilience to weather make it attractive to insurers, but its extreme weight and expensive, specialized installation raise replacement costs significantly. As a result, premiums may remain high despite the low risk of damage.

Wood shakes and shingles provide a natural, rustic look but are vulnerable to fire, rot, and insect damage. Even with fire-retardant treatments, many insurers consider them a higher risk, particularly in wildfire-prone areas. Homeowners with wood roofs may face higher premiums or limited coverage options.

Flat roofs, often made from materials like modified bitumen, TPO, or EPDM, are common in commercial and some residential properties. They are cost-effective but prone to drainage problems and water pooling, which can lead to leaks and costly repairs. Insurers may view them as higher risk unless well-maintained and located in dry climates.

Selecting the right roof type is about balancing appearance, cost, and long-term performance with insurance considerations. By understanding how each material is perceived by insurers, you can choose a roof that not only protects your home but also helps you secure better coverage terms and potentially lower premiums.

While the material and style of your roof are major considerations, insurers look at several other aspects that influence your risk profile and potential insurance costs. These factors provide a more complete picture of your home’s overall durability, susceptibility to damage, and the likelihood of future claims.

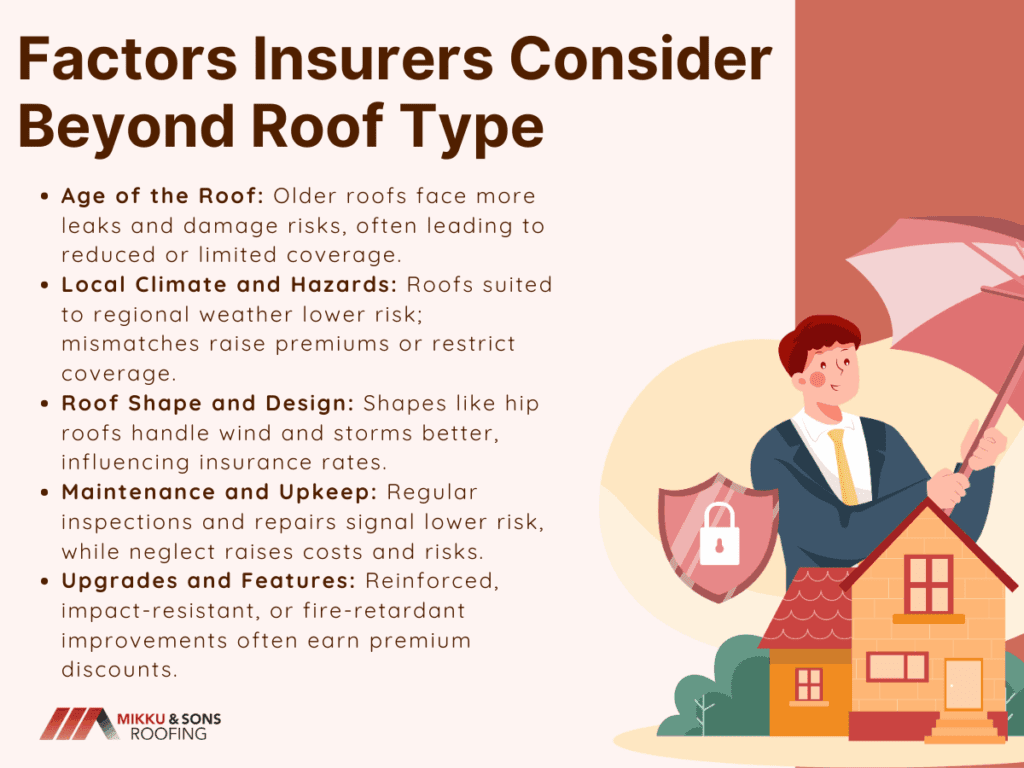

The age of your roof is a critical factor because older roofs are more likely to experience leaks, deterioration, and weather-related damage. Many insurers have age thresholds—often 15–20 years for asphalt shingles—beyond which they may reduce coverage or only pay the depreciated value in the event of a claim. Keeping your roof updated can help you avoid these coverage limitations.

Insurers consider the environmental risks your home faces, such as hurricanes, hailstorms, wildfires, or heavy snowfall. A roof that performs well in your region’s specific climate is seen as less risky, while a mismatch between roof type and hazard exposure can result in higher premiums or restricted coverage.

The shape and slope of your roof affect how it handles high winds, heavy rains, and snow loads. For example, hip roofs tend to fare better in strong winds than gable roofs, which can make a noticeable difference in insurance rates for storm-prone areas.

Insurers value evidence of regular roof inspections, cleaning, and repairs because they signal a lower risk of costly damage. Neglected roofs, on the other hand, increase the likelihood of water intrusion, structural issues, and higher claim frequency, which can raise premiums or limit coverage.

Adding features such as impact-resistant shingles, reinforced underlayment, or fire-retardant treatments can significantly reduce the chance of major damage. Many insurers offer discounts for these upgrades, especially in high-risk zones where prevention measures can save on future claim costs.

In short, insurers evaluate far more than just the material covering your home. By managing the age, design, maintenance, and protective features of your roof, you can strengthen your home’s resilience, improve your insurability, and keep insurance costs under control.

An insurance-friendly roof is one that minimizes the likelihood of damage, complies with safety standards, and demonstrates consistent, proactive care. Insurers reward roofs that reduce risk with better coverage terms, lower premiums, and even discounts.

Select roofing materials that are well-suited to your region’s most common weather threats, such as hail, high winds, or wildfires. Options like metal, slate, or Class 4 impact-resistant shingles can offer superior protection, longer lifespans, and a lower risk profile in the eyes of insurers.

Conduct regular inspections—ideally twice a year and after major storms—and keep documentation of all repairs, cleanings, and upgrades. Detailed records prove to insurers that your roof is properly maintained, which can help prevent disputes and support claims approval.

Don’t wait for leaks or structural issues to emerge before replacing your roof. Proactive replacement keeps your roof within the insurer’s preferred age limits and helps you qualify for replacement cost coverage rather than actual cash value settlements.

Adding Class 4 shingles, reinforced underlayment, or non-combustible materials can dramatically reduce damage from hail, high winds, or fire. Many insurers provide substantial discounts for these enhancements, especially in areas prone to severe weather or wildfires.

Ensure your roof meets or exceeds the latest building codes, particularly if you live in a region with special requirements for storm, seismic, or fire safety. Compliance shows proactive risk management and can prevent coverage issues during a claim.

A roof with proper drainage and ventilation is less likely to suffer from water pooling, mold growth, or heat damage. Installing or upgrading gutters, downspouts, and attic vents not only extends your roof’s life but also reduces the risk of costly insurance claims.

Small problems like loose shingles, minor leaks, or damaged flashing can quickly turn into major repairs if ignored. Promptly fixing these issues demonstrates responsibility to insurers and helps maintain your policy’s favorable terms.

Making your roof insurance-friendly is about combining smart material choices, diligent upkeep, and protective enhancements to reduce the likelihood of costly damage. By taking these steps, you can protect your home, strengthen your position with insurers, and potentially save money on premiums year after year.

Your roof is one of the most significant factors influencing your homeowners insurance, from the type of coverage you can get to how much you’ll pay for it. Insurers look beyond appearance, evaluating your roof’s material, age, condition, and ability to withstand local hazards. By understanding these considerations, you can make informed choices that not only protect your home but also position you for better coverage terms and potential cost savings.

The bottom line: a roof that’s durable, well-maintained, and hazard-appropriate benefits both you and your insurer. By selecting the right materials, following a consistent maintenance routine, and investing in upgrades that enhance safety and resilience, you can lower your risk profile, improve your policy options, and enjoy greater peace of mind knowing your home is well protected.